Europe’s new energy project promises to put a focus on consumer interests, yet what this new market would look like in practice is often poorly understood. As the European Commission ponders the design of a new and interconnected energy market for Europe, it needs to make sure this market benefits consumers, while not disadvantaging suppliers. Phil Baker, senior advisor at the Regulatory Assistance Project, explains how this can be achieved.

By managing electricity consumption in response to price signals, customers can, either directly or through a third party, participate in the market and benefit from lower power costs. New analysis demonstrates that these benefits could be significant and are likely to increase over time as Europe moves to deliver its decarbonisation goals. However, these consumer benefits could be jeopardized by the treatment of “supplier compensation,” an issue that arises from the relationship between customers, their suppliers, and any third-party aggregators involved in assisting customers in managing their energy services. Aggregators play a critical role by “bundling up” the demand flexibility of many smaller customers to deliver valuable services to the market at scale. Getting the “supplier compensation” issue right could improve European energy security and save consumers billions of euro annually in coming years.

The Societal Benefits of a Flexible Energy Market

In order to more fully understand the potential benefits of customers managing their electricity consumption, RAP commissioned an analysis of the impact of demand response on the French, German-Austrian, and Nordic day-ahead markets. The analysis demonstrates that all power customers benefit from increased consumer market participation and that, while varying from year to year, the potential benefits are considerable.

This is illustrated in the figure above, which shows the predicted reduction in the French, German-Austrian, and Nordic day-ahead market revenues due to the application of demand response. Depending on the level of demand response assumed (how much and for how many hours), the cost to suppliers in sourcing energy for their customers could be reduced by as much as €1600 million across the three markets. Assuming sufficiently competitive retail markets and/or adequate regulatory oversight, these savings should be passed through to customers in the form of lower retail prices.

The Issue of Supplier Compensation

When customers, or third-party aggregators operating on their behalf, modify their consumption to offer services to the market, suppliers argue that energy purchased in anticipation of customers’ needs is effectively “sold-on” in the form of demand response. As suppliers cannot generally bill customers for energy they don’t consume, an individual supplier may appear to face a loss. This apparent loss of income has resulted in demands by suppliers to be compensated, either by negotiated agreement with the customer or his third-party aggregator, or as determined by a nationally administered arrangement as is the case in France.

However, as the actual cost of the energy sold-on by the customer will be known only by the supplier, negotiated compensation is inherently unfair. This “information gap,” when coupled with the fact that, in many Member States, customers or their aggregator must have permission from the customer’s supplier before providing demand services, places suppliers in a very dominant negotiating position. The administered approach to compensation adopted by France and suggested by some as a model for Europe as a whole, is an attempt to overcome these difficulties. However, the RAP analysis shows that direct compensation by aggregators, even via an administered arrangement, is likely to hinder the deployment of demand response. Customers or aggregators would pay almost as much, or more, in compensation to suppliers as they could realize from delivering demand response services. Little, if any, revenue would remain to cover the costs of establishing the capability in the first place or making any reasonable return, therefore destroying the case for further deployment. This conclusion is confirmed by evidence from France where, since 2014, some 80 to 87 percent of all demand response revenues have been taken up by compensation payments. The revenue remaining averaged some €7/MWh, insufficient to meet operational let alone capital costs.

A Simple Alternative

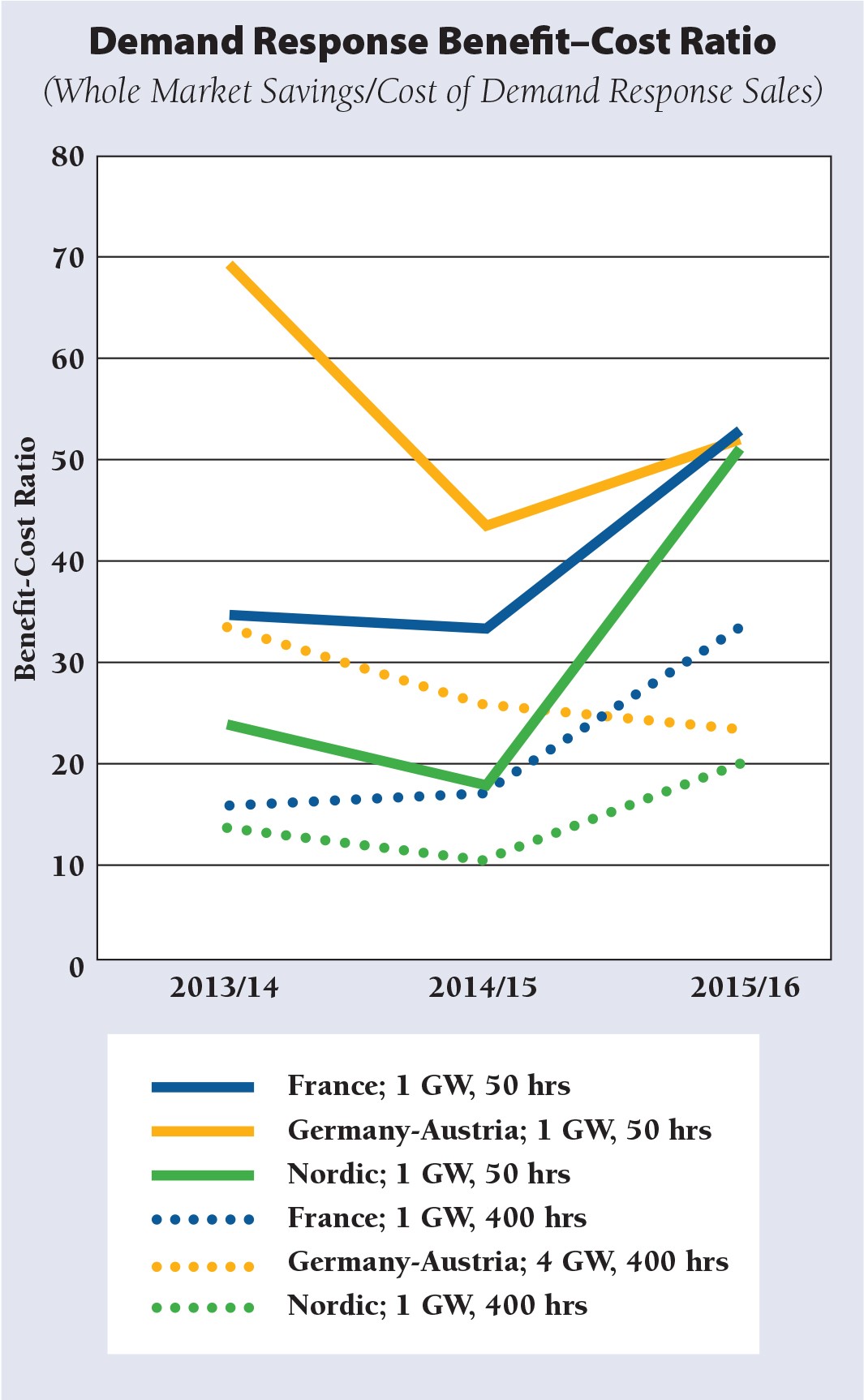

As demand response reduces the costs incurred by suppliers in sourcing energy for their customers, demands for direct compensation are not only counterproductive but also unjustified. A more obvious arrangement would be for suppliers to simply retain some of the savings delivered by demand response to cover any lost income, rather than passing all those savings through to customers or insisting on full supplier compensation from those customers who are delivering the savings. This becomes even more obvious when one considers that the costs incurred by suppliers are only a tiny fraction of overall benefits to their customers. In the scenarios RAP investigated, the savings from demand response exceed the likely costs to suppliers by a factor of at least 10 and as high as 70. Over time, as intermittent renewable capacity grows and energy prices become more volatile, the ratio of savings to cost can be expected to increase even further, providing more than enough headroom for suppliers to recover any lost income by this means.

Conclusions

Customer participation in the electricity market though managing consumption can deliver real benefits for all consumers. For the scenarios assumed in the analysis reported here, annual savings in consumers’ energy costs across the French, German-Austrian, and Nordic markets could amount to €1.6 billion—clearly, the savings to be achieved across the whole of Europe would be even more significant. It is also likely that potential savings will increase steadily over time with the continued deployment of intermittent generation and increasing energy price volatility.

However, these potential savings could be lost if customers, or aggregators operating on their behalf, are required to compensate suppliers directly for energy bought upfront but sold-on and not billed. Direct compensation, either via negotiation or administered arrangement, is both counterproductive and unnecessary. The total savings seen by suppliers will always significantly exceed any loss of revenue, and a more obvious solution would be for suppliers to simply retain some of those savings. This would allow suppliers to remain financially whole, while at the same time facilitating the development of flexible demand, allowing customers to retain nearly all of the associated benefits and lowering the cost of decarbonisation.

Given the importance of demand flexibility to the cost-effective delivery of Europe’s energy policy goals, we urge the Commission and other EU entities to support its deployment by adopting a balanced approach to supplier compensation as they develop new proposals on power market design.