Beginning in the 1970s, the U.S. electricity industry experienced a wrenching transformation from a sector characterized by high growth to one focused on reliability, economic efficiency, and environmental performance. The contemporary building blocks of electricity planning in the United States emerged during this time period. Despite changes in the industry, including the emergence of organized markets, many of these building blocks are still in use.

China’s electricity sector is about to undergo its own version of this transformation. In China, a combination of slowing electricity demand growth, public and policy demands for cleaner air, and high costs are driving a similar transition from high growth to a new paradigm oriented around economic efficiency and environmental performance. A key difference in China’s case is that this transition is occurring at the same time that the country is making large policy-driven investments in wind, solar, and hydroelectric energy.

Electricity Planning, part two of the technical primer Integrating Renewable Energy into Power Systems in China, provides an overview of the challenges that current approaches to electricity planning in China pose for integrating renewable energy into the country’s power systems. As the report describes, many of these challenges are rooted in the larger paradigm shift in China’s electricity sector.

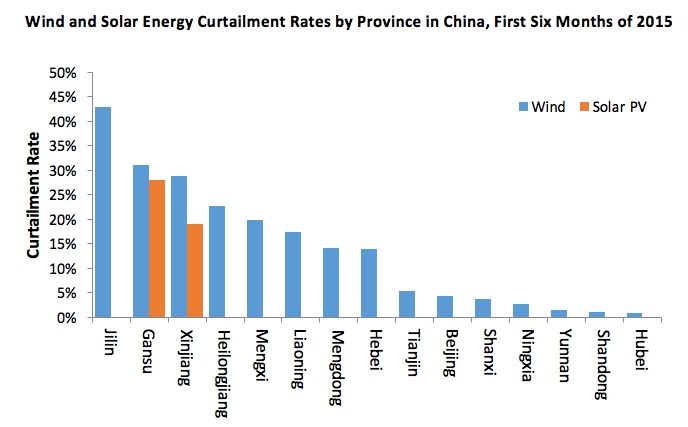

High rates of renewable energy curtailment—the share of renewable generation that is effectively discarded—are the clearest indicator of renewable integration challenges in China. In the first six months of 2015, eight provinces had wind curtailment rates higher than ten percent, with the highest reaching more than 40 percent; the two main solar generating provinces had solar curtailment rates of 19 percent and 28 percent, respectively. By way of comparison, wind and solar curtailment rates in the U.S. are typically less than 1 percent.

Some of China’s renewable integration challenges can be addressed through changes in operating practices, as described in the first primer in this series. Others must be dealt with through improvements in planning.

The following example illustrates the role and importance of planning for renewable integration in China. Provincial grid companies are ultimately responsible for physically balancing electricity demand and supply on the grid at all times to maintain grid reliability. However, neither provincial planning agencies nor grid companies have historically had a planning process to determine the “right” amount of generation capacity to meet reliability needs, and there are neither planning processes nor market price signals to guide where new investments are made (e.g., in renewable, gas, or coal power plants).

These gaps were often concealed in a high-growth environment. As demand growth has slowed, however, they are becoming more apparent. For instance, the lack of a reliability planning process to determine the need for new generation capacity has led to an overbuilding of coal-fired generation capacity. Rather than retiring or temporarily closing (“mothballing”) unneeded power plants, planners reduce operating hours for all generators, decreasing all generators’ profits but allowing a larger number of them to remain solvent. These reductions in operating hours also apply to wind and solar generators in the form of curtailment, contributing to the problem shown in the figure above.

More broadly, Electricity Planning identifies four kinds of planning improvements that would facilitate the integration of higher penetrations of renewable energy into power systems in China:

- Generation Planning: ensuring a better match among generation investment, generator approval, and the generation capacity needed to reliably meet demand, and facilitating a more flexible, lower-cost generation mix;

- Transmission Planning: better integrating generation planning into transmission planning, and encouraging a more economically efficient expansion of the transmission system;

- Environmental Planning: better integrating environmental goals into electricity planning and resource procurement; and

- Organizational Capacity and Information Access: strengthening the capacity and expertise of regulatory organizations, and encouraging greater transparency and wider access to information that will assist in decision-making.

These improvements should be part of the larger transition in China’s electricity sector, toward economic efficiency and environmental performance. They are important even outside of renewable integration considerations. China’s recently restarted electricity reforms provide an opportunity to make these kinds of planning improvements.