The European Council’s proposals on the internal energy market fundamentally weaken the framework that is needed to deliver an integrated market that will benefit European energy consumers, write Philip Baker and Christos Kolokathis from the global energy policy advisors Regulatory Assistance Project (RAP). The proposals may even legalise practices that are currently — and should remain — illegal. The authors call on European policymakers to support the European Commission’s proposals in the Clean Energy Package.

Europe can deliver enormous benefits to its electricity consumers by accelerating progress toward an integrated internal energy market. There are three key pathways for unlocking this potential, all involving a more regional approach to operating Europe’s electricity grid. These are: increasing the interconnector capacity made available to the markets and taking a more collective or regional approach to both assessing resource adequacy and energy balancing.

The European Commission’s Clean Energy for All legislative package (CE4All), published on 30 November 2016, represents significant progress in the right direction. The Commission’s proposals are now being negotiated by the European Parliament and the European Council (the Member States). The outcome of this process will make or break progress on the EU’s energy market integration for the next decade. Unfortunately, counterproposals made by the European Member States threaten to halt progress — or even reverse it.

Market integration lowers costs

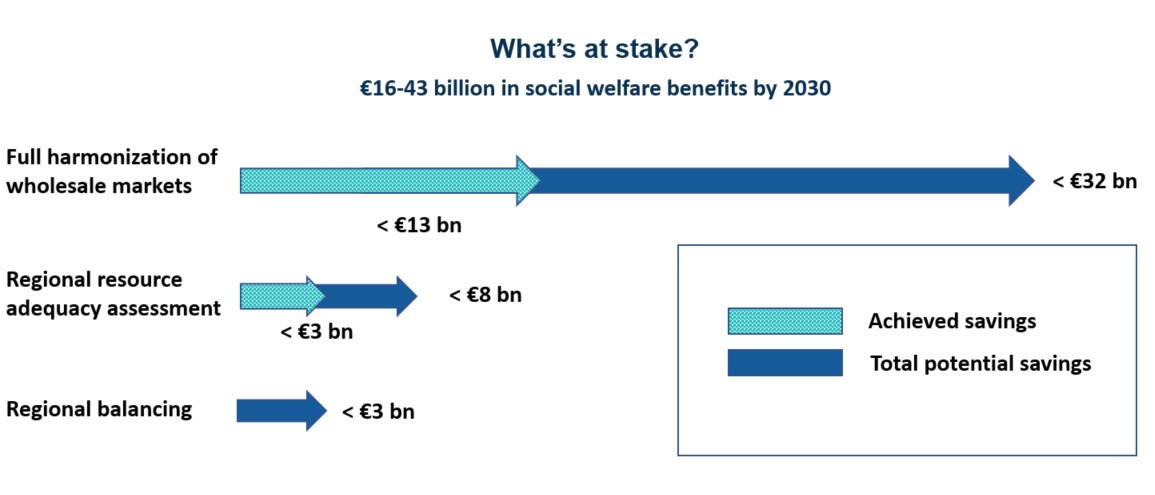

Regionalisation will have many benefits — allowing customers to access the cheapest sources of energy, pooling risk and exploiting geographic diversity, and reducing the need for new generation capacity. Estimates by Booz & Co. and others suggest that the increase in social welfare of fully integrating Europe’s electricity markets, some of which has already been achieved through market coupling, could lie in the range of €16 to €43 billion per year by 2030.

The magnitude of future savings depends on the extent to which Europe’s generation portfolio can be optimised and the necessary interconnector capacity developed. As shown by the chart below, the bulk of these savings will be accrued by harmonising and lowering wholesale energy prices, with smaller but still significant savings arising from a more regional approach to resource adequacy and balancing.

While investment in new capacity will be required, there is considerable potential to increase the utilisation of existing interconnector capacity.

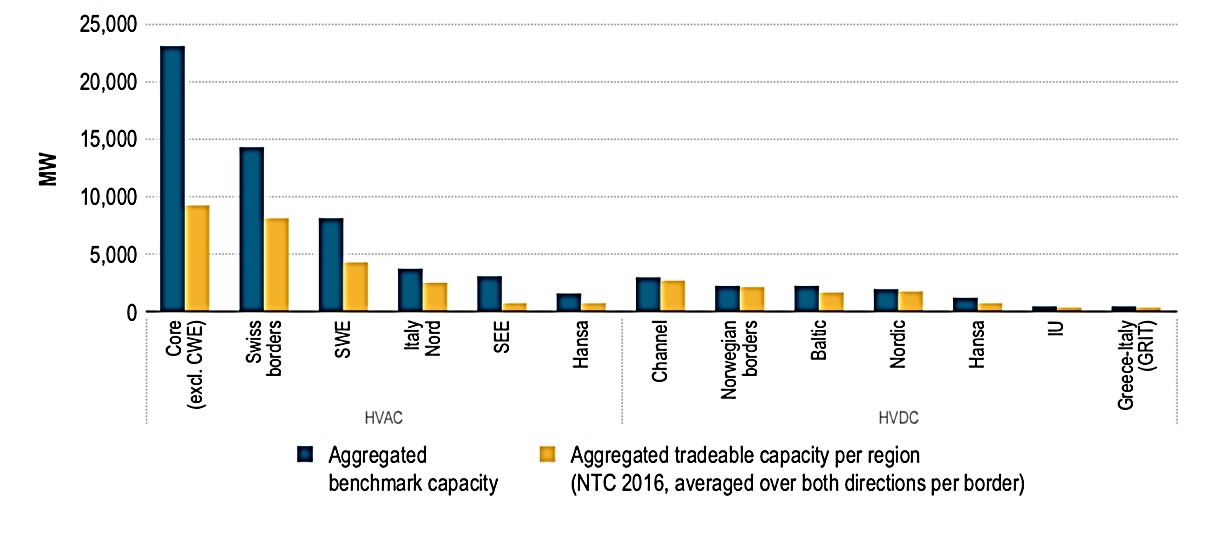

Analysis by the Agency for the Cooperation of Energy Regulators (ACER) shows, as depicted below, that only around one-third of the realistically available cross-border capacity is currently offered to the market in the Core — excluding the Central Western — region, which covers the majority of continental Europe.

In some instances, the capacities offered are even lower. For example, Germany limits imports from the Netherlands to some 12 percent of available interconnector capacity, while the Netherlands manages to allow 83 percent for flows in the opposite direction.

Aggregated tradeable interconnector capacity compared with benchmark. ACER/CEER 2017

The low level of interconnection capacity made available to the wholesale markets results, to a large extent, from the practice of reducing congestion within national borders by limiting cross-border flows.

Despite the fact that Article 16 of Regulation EC 714/2009 prohibits “moving internal congestion to the borders,” ACER’s analysis shows that the practice is widespread. This is all the more remarkable given that the practice is analogous to imposing a cap on cross-border trade in goods in order to protect the interests of a particular Member State — a practice that would not be tolerated in any other area of the European Single Market.

Council’s proposal reverses progress on interconnector usage

In Article 14 of the Regulation on Electricity Markets, the Commission proposes to address this situation by stipulating that redispatch and countertrading (i.e., adjusting generation schedules to manage internal congestion) should be used to maximise cross-border capacity, provided that it is economically beneficial to do so “at a Union level.”

However, the Council has proposed that the increase in interconnection capacity offered to the market should be allowed to follow a linear progression, starting at the level of capacity offered at the point of enactment and rising to 75 percent of available capacity after four years, or by 2025.

It is also interesting to note that, of the Member States that assume zero or little interconnector contribution, five are implementing or planning to implement capacity mechanisms.

This represents a significant retreat from the current legal position, which is that interconnector capacity offered to the market should be maximised and should not be reduced by “moving internal congestion to the borders” — subject to grid security not being compromised. In addition, the proposal seems entirely arbitrary and could encourage Member States who currently limit interconnector capacity to delay taking action, thus ensuring they have a low baseline for the proposed linear progression.

The Commission’s original proposal should therefore be supported and the Council’s counterproposal rejected.

It is also important to rigorously enforce existing legislation that prohibits moving congestion to the borders. If a Member State seeks to be released from this requirement, it should be required to demonstrate that the costs exceed the regional benefits or that security would be compromised.

This legislation should protect the interests of Europe’s electricity consumers as a whole, rather than those of any individual Member State.

Regional assessment of resource adequacy necessary

While some Member States are forecasting capacity deficits in the years ahead, others are forecasting surpluses. Taking Europe as a whole, most Member States are situated in regions with a healthy resource adequacy situation. Aggregating these surpluses and deficits over appropriately defined regions will reduce the overall need for investment in new resources. At the same time, it will allow supply reliability to be maintained at a lower cost than would be the case if Member States continue with a “self-sufficiency” approach.

Member States therefore need to take appropriate account of potential support from neighbouring systems when assessing security of supply.

While responsibility for security of supply remains a matter for individual Member States, this responsibility needs to be squared with the benefits to those same Member States and their consumers from a more collective approach to resource adequacy assessment in order to realise the potential savings in investment costs. Member States therefore need to take appropriate account of potential support from neighbouring systems when assessing security of supply.

To some extent this already happens. However, ACER’s 2017 Market Monitoring Report exposes the wide disparity in the extent to which interconnection contribution is taken into account. ACER’s analysis shows that, out of 21 Member States surveyed, ten did not take any account of interconnection contribution to resource adequacy. Among the remainder, the extent to which interconnector contribution was taken into account varied widely.

It is also interesting to note that, of the Member States that assume zero or little interconnector contribution, five are implementing or planning to implement capacity mechanisms. This begs the question: Would those mechanisms be necessary if proper account were taken of potential interconnection contribution?

Clean Energy for All package mixed on shift to regional resource adequacy

The failure of Member States to fully take into account interconnector contribution to resource adequacy creates a risk of unnecessary investment in generation capacity — costs that will be borne by electricity consumers.

The Council’s proposal therefore risks failure to deliver the benefits that a more coordinated resource assessment could bring.

Furthermore, the wide disparity in the level of contribution assumed underlines the need for a common methodology and a coordinated approach to analysis across the internal energy market. The Commission’s CE4All package recognises the need for a coordinated approach, with Article 18 of the recast Regulation proposing that Member States monitor capacity requirements based on the Europe-wide assessment carried out by the European Network of Transmission System Operators, ENTSO-E.

In addition, Article 22 proposes that non-domestic generation capacity should be allowed to participate in capacity mechanisms and that the Regional Operational Centers (ROCs) have a meaningful role in deciding on the level of participation.

The Commission’s proposals for a coordinated approach should be supported. The introduction of a European, or preferably a regional, resource adequacy assessment would allow capacity surpluses and deficits to be aggregated on a regional basis, raising the value of existing resources and reducing the need for investment in new resources.

By contrast, the Council’s watered-down proposal would allow Member States to continue to assess capacity requirements on a national basis, albeit “taking note” of any European assessment and opinion issued by ACER. The Council’s proposal therefore risks failure to deliver the benefits that a more coordinated resource assessment could bring.

Regional electricity balancing most effective approach

The need to minimise imbalance costs will assume increasing importance as the deployment of wind and solar continues, and balancing energy over wider areas will allow geographic and technical diversity to be exploited, reducing balancing volumes.

While analysis suggests that the potential savings in balancing costs will be relatively modest compared with savings from market integration and a coordinated resource adequacy assessment, the savings to be achieved by balancing across wider areas are still significant at about €3 billion per year by 2030.

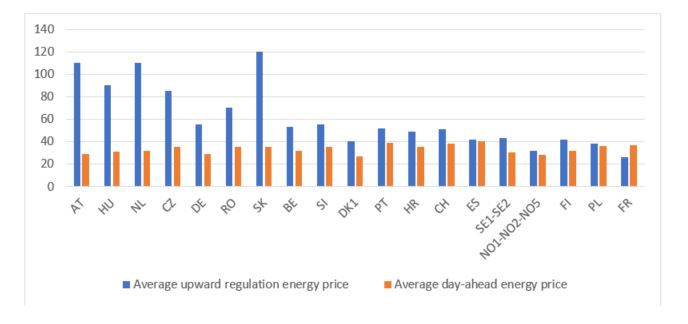

There has been relatively little progress in coordinating national balancing activities in Europe. In fact, analysis shows that imbalance price differentials are far greater than in the day-ahead and intra-day markets. These price differentials are significant for a number of reasons. Imbalance prices ultimately provide a cap or collar on day-ahead and intra-day prices and therefore will impact the extent to which these prices can be harmonised across Europe. Furthermore, unnecessarily high imbalance prices — i.e., where prices are inflated due to a lack of competition or liquidity — represent a barrier to market entry, particularly for small entities and for intermittent renewable resources, which cannot easily respond close to real time.

Difference in upwards balancing energy price and day-ahead energy price, 2016 ACER/CEER 2017.

The Commission’s Clean Energy for All package

Article 5 of the Commission’s recast Regulation on energy markets proposes that balancing and reserve capacity should be calculated and procured on a regional basis. In addition, Article 34 requires that ROCs have a meaningful role in these activities. This is eminently sensible and necessary if the benefits of balancing over wider areas are to be realised, and the Commission’s proposal to regionalise these activities should be supported.

Unfortunately, however, the Council is resisting a more regional approach and has proposed that transmission system operators (TSOs) continue to be responsible for balancing requirements, although noting that this “may be facilitated on a regional level.” Exactly what this means is unclear.

What is clear, however, is that unless reserve and balancing capacity requirements are assessed at a regional level and procured via a regional platform as proposed by the Commission, the potential cost savings associated with energy balancing and the integration of renewable resources will not be realised. The Council’s position, that balancing remains a TSO responsibility, with ROCs having no meaningful role and unable to apply their regional focus and expertise, risks placing these savings out of reach.

Don’t lose sight of the forest for the trees

When considering specific issues related to power market and system operation, it is easy to lose sight of the overall benefits to consumers that regionalisation and market integration can deliver.

We must be aware of those benefits and recognize the fundamental importance of regionalisation and market integration in the cost-effective, reliable transition to a decarbonised power sector. The Council’s position, at best, waters down the Commission’s proposal and perpetuates the status quo. At worst, it represents a large step backward.

A version of this blog was originally published by EnergyPost.