Electricity generators often claim that prices cannot fully reflect the value of the reliability they offer the market. Hence they insist they need separate capacity payments to justify investments. But according to Mike Hogan, the current energy market design is fully able to reflect the value of reliability, even if it doesn’t always do so in practice. In a new report, he describes a smarter approach, one that can ensure reliability in a low-carbon power system at the lowest cost to consumers, without need for capacity markets.

Energy markets are often said to suffer from a “missing money” problem, referring to the idea that, for various reasons, prices in the energy market do not fully reflect the value of investment in the resources needed to meet expectations for reliability. While the analysis behind these claims is often muddled, there can be legitimate concerns about the quality of implementation of markets and whether they are adequately remunerating needed investment. RAP’s new report, Hitting the Mark on Missing Money: How to Ensure Reliability at Least Cost to Consumers, explores the topic in depth for a non-specialist audience, arriving at a set of recommendations for how electricity markets can meet expectations for reliability at least cost in the transition to a low-carbon power system.

There are different pathways to a reliable power system, some more costly than others. Measures to address the missing money problem must address the entire objective—to ensure reliability at the lowest reasonable cost. Many of the remedies proposed to address missing money, in particular the various out-of-market “capacity remuneration mechanisms,” run the risk of creating a different problem, one borne principally by consumers: misallocated money, overcompensating some resources and undercompensating others.

Energy Prices in Energy Markets

Misguided approaches to the missing money problem often originate in a flawed understanding of how energy prices are meant to be formed in the energy market and how they are expected to support needed investment. It is often claimed that energy prices reflect only the instantaneous demand for energy and are limited by the short-run production cost of the highest cost generation to clear the energy market. It is then argued that, since this is the case, some form of additional payment is needed to support investment in reliability, especially as the resource mix shifts to capital intensive, low-operating cost resources.

There are big problems with this narrative. The power industry has always been capital intensive. Most highly capital intensive industries—e.g., airlines, real estate, and oil refining—operate on the basis of unit prices. And it’s missing some crucial pieces of how energy markets are meant to set prices. In every hour, prices should reflect the fact that the demand for energy and the demand for balancing services compete for the same pool of system resources. Furthermore, in hours when supply margins are tight, system operators take a sequence of actions with marginal costs well in excess of the short-run production cost of the last kWh to clear the energy market. Energy prices should reflect that as well.

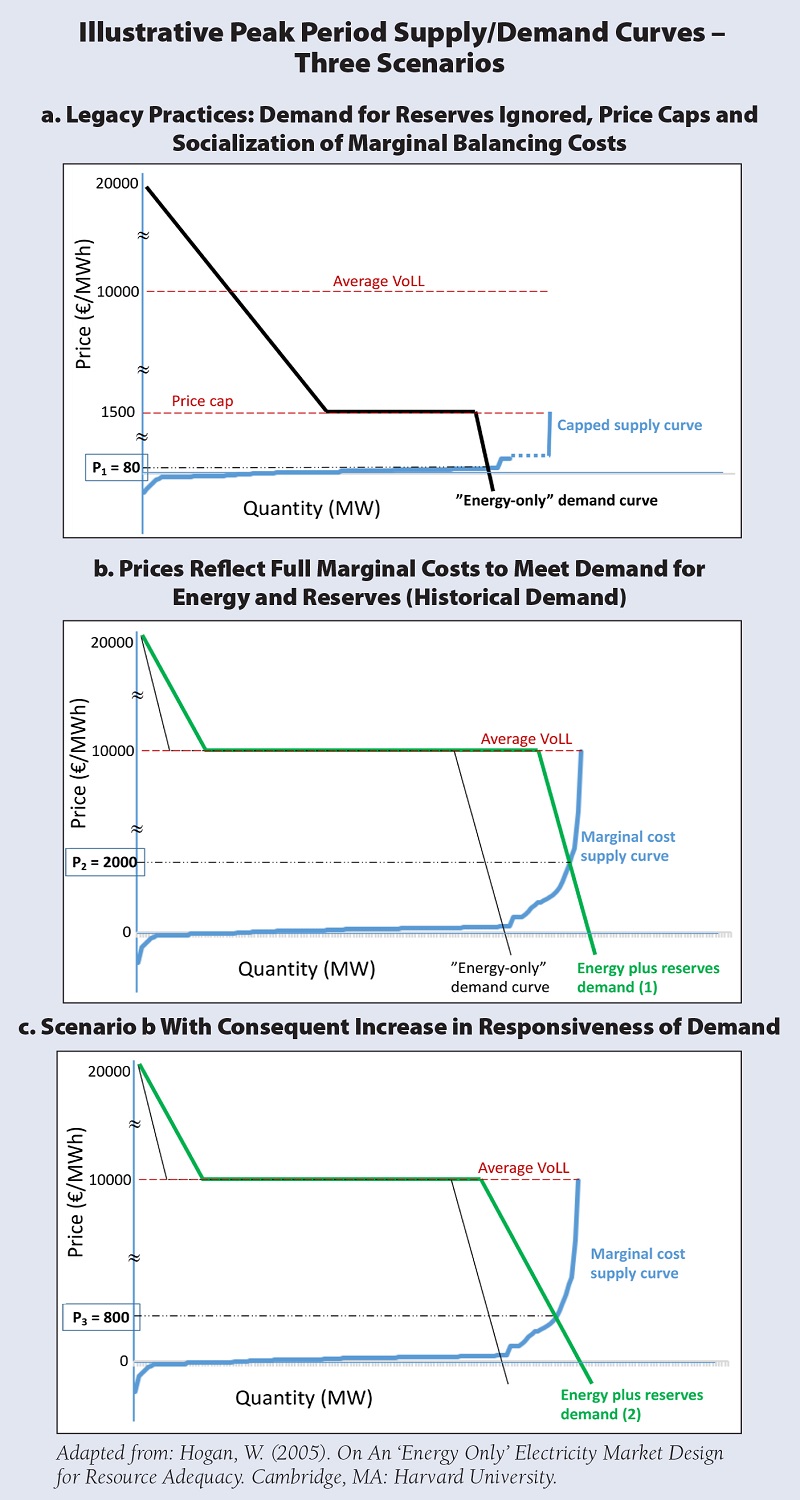

However, it is true that energy prices in many markets today are distorted by legacy practices that socialize or ignore the marginal costs of actions taken by system operators during periods of tight supply margins, and that fail to reflect the price system operators should charge in any given hour to release scarce reserves to meet increased demand for energy (See Figure 1). For example, less flexible generators are often paid separately for the extra costs they incur to be available when needed rather than having to recover those costs through their market offers. When such factors are properly reflected, prices can rise to levels many times the short-run production cost of the last kWh to clear the energy market, reflecting the actual cost of reliable energy. This is how the energy market is meant to value the investment needed to meet consumer expectations for reliability, with or without renewables.

Figure 1

Thus, as in any healthy commodity market, energy prices can support needed investment both directly and, as importantly, by exposing wholesale market participants to the risks associated with periods of supply shortage and supply surplus. Buyers exposed to risks of higher and more volatile prices should be expected to manage those risks by entering into forward-looking commercial arrangements with producers directly and indirectly, via bilateral contracts and traded hedging products. These arrangements provide long-term support for the investment needed to ensure reliability.

Theory vs. Practice

As noted, in practice many energy markets currently fall short of this ideal, which is why judicious administrative and regulatory interventions can be appropriate. Electricity is an especially important commodity with its own particular characteristics. First is the difficulty in storing electricity at an affordable cost, which leads to the risk of price gouging by withholding production. Second is the historical tendency for electricity demand to be relatively “inelastic,” unresponsive to real-time conditions of either surplus or scarcity. To address these concerns, market operators have employed, among other measures, price caps and socialization of the costs of emergency measures. As a result, clearing prices in energy markets often fail to reflect the real cost of actions required to “keep the lights on” and the true value of uninterrupted service to end-use consumers.

Table 1

![]()

That value can be high—much higher for many services than is currently reflected in most markets during shortage periods—but it is not unlimited. System operators, operating in the background, act on behalf of consumers to position the resources necessary from one hour to the next to meet the demand for both energy and reliability. In doing so, they apply a standard, usually imposed by civil authorities, that balances the value of continuous service against the costs of ensuring it. The result is a cost that system operators charge, or should charge, to relinquish reserves when the demand for or the availability of energy pushes the system close to its limits. In this way the system operator, acting in effect as the buyer or seller of last resort, bridges the gap between the theoretical ideal for an electricity market and the current practical reality. As described below, extending this administrative role to an administrative remedy for restoring missing money to energy market prices represents an excellent option for addressing the problem.

Capacity vs. Capability

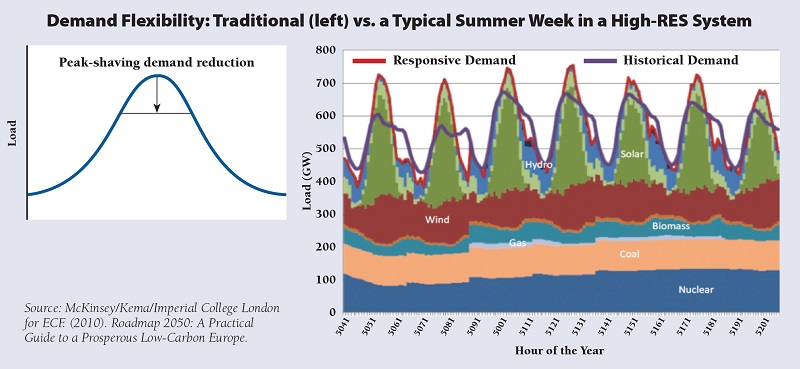

In addressing concerns about missing money, it is important to ask what kind of capacity resources the proposed remedies are remunerating. As we move farther down the road to a decarbonized power system, one point on which there is nearly universal agreement is that the system will need to become more flexible both on the supply side and on the demand side. Remedies that fail to recognize this, especially remedies that reward capacity resources without regard to their operational capabilities, can lock in the legacy mix of resource capabilities and retard the transition to a more flexible system. Remedies that effectively exclude non-traditional resources, especially innovative new demand-side technologies, will overlook some of the most effective and cheapest alternatives for delivering the needed flexibility.

Figure 2

Flexibility is different from capacity. The definition of a unit of firm or reliable capacity is well developed and will remain constant regardless of how the resource portfolio evolves. Flexibility defies clear definition. It may be an increase or a decrease in supply (or a decrease or increase in demand), over milliseconds or minutes or hours or days. The best sources for some kinds of flexibility are usually not the best sources for others. And the portfolio of flexibility valuable to the system will evolve continuously depending on which low-carbon pathway is chosen and how the technologies evolve. Fully formed energy prices are the clearest expression of what flexibility the system needs and what it’s worth. Measures that divert revenues from energy prices to out-of-market mechanisms degrade that functionality. It is difficult to envision an out-of-market remuneration mechanism capable of matching the effectiveness of fully formed energy prices in valuing investment in flexible capacity resources.

A Smart Strategy for Tackling Missing Money

We propose a response to the missing money problem that is effective, efficient, and durable. That response must begin with the setting of an economically rational standard for reliability and an independent process for determining what investment is actually needed, incorporating opportunities for energy efficiency and flexible demand. “Keeping the lights on” is about more than just reliability, it’s about delivering consumers value for money. Sometimes claims of “missing money” are just rent-seeking in disguise.

The tendency in many jurisdictions has been to default immediately to what is actually the third-best option, out-of-market capacity mechanisms. If this is ultimately deemed necessary, it should be a supplement to rather than a substitute for the first- and second-best alternatives described below; it should recognize and reward resources based on desirable capabilities to the extent possible; and it should be designed with the objective of eventually phasing it out.

The first priority should be to identify and redress root causes. These tend to range across several categories:

- Price controls to compensate for failure to establish institutional frameworks and processes needed to ensure effective competition;

- Failure to reflect the demand for balancing services in energy market clearing prices and socializing the real-time costs of providing those services;

- Maintaining traditional market rules and procedures that exclude non-traditional sources of the services needed to maintain reliability; and

- Failure to anticipate and correct for unintended consequences of good policies, such as overcapacity driven by the need to support deployment of new zero-carbon supply.

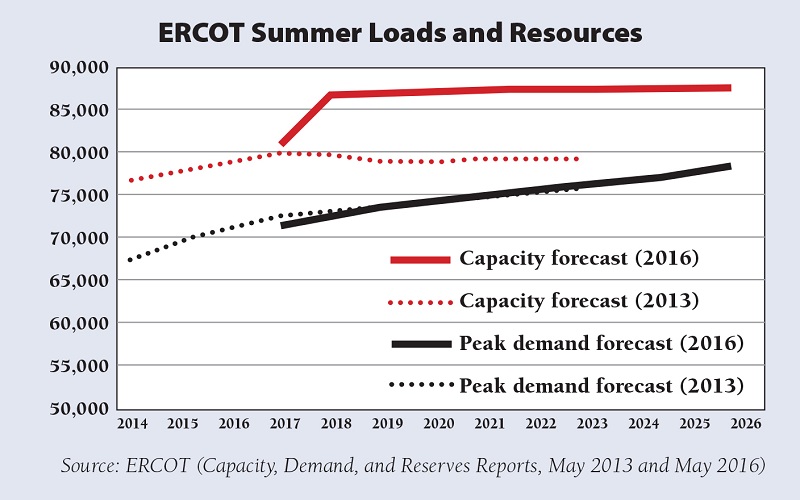

While these are common themes in most markets, identifying and rooting out specific problems will take time. In the meantime, some form of administrative market mechanism may be useful. Thus, the second priority, to be pursued in parallel with redressing flaws in the implementation of the energy market, should be developing administrative mechanisms designed to adjust prices in the energy and balancing services markets if and when they fail to reflect the real cost and true value of energy and balancing services, particularly during periods of shortage. There are multiple examples of mechanisms in operation, ranging from the Great Britain, PJM, and ISO New England markets, where they operate in parallel with out-of-market mechanisms, to the ERCOT market, where this is the principal administrative mechanism deployed to ensure reliability.

Figure 3

There is good evidence that these two strategies, deployed in tandem, can address legitimate concerns about needed investment. They should be given an opportunity to do so, particularly where the need for more generating capacity remains years in the future, as is the case in most of Europe and North America. They offer the best chance to deliver not just reliability, but reliability at the lowest reasonable cost.

A version of this post originally appeared in Energy Post.